Home » Credit Cards » Penalty APRs: What Are They and How to Avoid Them

Whether you’re carrying a balance or just want to avoid trouble, knowing when and why a penalty APR applies could save you hundreds of dollars.

Advertiser Disclosure: Our first priority is to provide valuable information to help our readers gain insight into financial topics. Although we receive compensation from some of the brands listed on our site, we only highlight companies we believe can benefit our readers and their financial situations. Consumer Insite has partnered with CardRatings for our coverage of credit card products. Consumer Insite and CardRatings may receive a commission from card issuers.

High interest rates can make credit card debt grow fast, but what happens when those rates suddenly spike even higher? That’s where penalty APRs come in. Understanding how they work can help you avoid unexpected costs and protect your financial progress.

What is a Penalty APR?

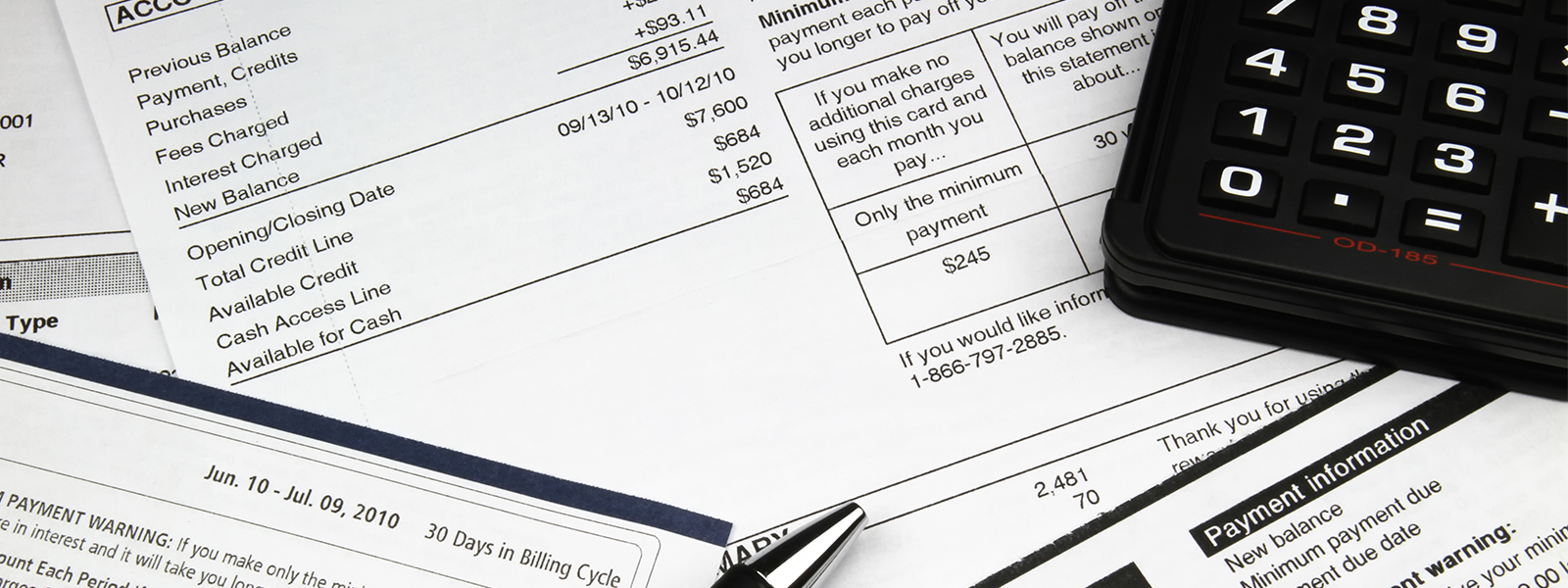

A penalty APR is a higher interest rate that your credit card company may apply if you violate the terms of your cardholder agreement. While a standard APR might range from 16% to 24%, a penalty APR often jumps to 25% or higher, sometimes up to 30%. This higher rate increases the cost of carrying a balance and can lead to growing debt quickly if not addressed.

Unlike a regular APR, which applies based on your credit score and payment history at the time you opened the account, a penalty APR is a reactive rate. Lenders use it to discourage risky behavior, like missed payments. If triggered, it doesn’t just apply to future purchases—it may also impact existing balances, depending on your card’s terms.

When Does a Penalty APR Kick In?

Penalty APRs typically activate when you miss a payment, pay late, or exceed your credit limit. Even one missed due date can be enough for your issuer to raise your rate. Some cards also apply a penalty APR if your payment is returned due to insufficient funds.

These triggers can happen easily, especially if you’re managing multiple cards or forget to schedule a payment. Once the penalty APR is applied, your account may be flagged for risk, and the higher rate can remain in place for months—even after the issue is resolved. To avoid this, it’s important to monitor your due dates, stay within your credit limit, and keep your payment method updated.

Penalty APRs don’t go away overnight. Under the Credit Card Accountability Responsibility and Disclosure (CARD) Act, issuers must review your account after six months of on-time payments if a penalty APR was applied. However, that doesn’t guarantee a rate reduction.

Some credit card companies may keep the higher rate in place indefinitely, even after consistent payments. Others may remove it sooner as a courtesy, but that’s up to the issuer. If you’ve triggered a penalty APR, it’s worth contacting your card provider to ask about the steps required for reinstating your original rate.

How Does a Penalty APR Affect Your Credit Card Balance?

When a penalty APR takes effect, the cost of carrying a balance can rise fast. More of your payment goes toward interest and less toward reducing your principal. That means even if you’re paying the same amount each month, your balance may shrink more slowly—or not at all.

This higher rate can make it harder to get ahead financially, especially if you’re already managing debt. Over time, it can add hundreds of dollars in extra interest and make it more difficult to meet other financial goals. Avoiding a penalty APR can help you keep control of your monthly budget and long-term payoff plans.

Can Penalty APRs be Applied to Existing Balances?

In many cases, a penalty APR only applies to new purchases made after the rate kicks in. However, that’s not a universal rule. Some credit card agreements allow issuers to apply the penalty rate to your existing balance if it’s clearly disclosed in the terms and conditions.

If you’re unsure how your credit card handles this, check your cardholder agreement or contact customer service. Understanding the fine print can help you plan ahead and avoid costly surprises if a payment slips through the cracks.

How to Know if You’re at Risk of a Penalty APR

You don’t have to wait until it’s too late to spot trouble. If you’ve missed a payment, come close to your credit limit, or had a returned transaction, your account may already be flagged for a penalty APR. Reviewing your monthly statements can help you catch warning signs early, such as late payment notices or increased interest rates.

Set up calendar reminders, enable text or email alerts, or enroll in auto-pay to make sure payments are made on time. It’s also a good idea to revisit your credit card agreement periodically. The fine print defines exactly what actions could trigger a penalty APR, so you know what to avoid.

Tips to Avoid Triggering a Penalty APR

Staying organized is the best way to keep penalty APRs off your radar. Start by making sure you always pay on time—even if it’s just the minimum amount due. Setting up automatic payments or due-date alerts on your phone can help prevent missed deadlines.

Keep your balance well below your credit limit to avoid over-limit fees or flagging your account as high risk. If you carry multiple cards, track due dates separately to prevent any slip-ups. A little preparation goes a long way in protecting your interest rate.

Can You Reverse a Penalty APR?

A penalty APR isn’t necessarily permanent. If it was triggered by a one-time mistake, contact your credit card issuer and ask if they’ll make a courtesy adjustment. Some issuers may be willing to reverse the rate, especially if you’ve had a good payment history in the past.

Even if they won’t remove it immediately, you can work toward reinstating your regular APR. Make six months of on-time payments and check in with customer service again. In many cases, showing that the issue was temporary is enough for them to lift the penalty.

Comparing Credit Cards With and Without Penalty APRs

Not all credit cards charge a penalty APR. Some issuers advertise cards without this feature, offering more flexibility for consumers concerned about missing a payment. These cards may offer a flat-rate APR regardless of payment history, which can help minimize the financial impact of an occasional mistake.

Before applying for a new card, review the terms and conditions carefully. Look for language about penalty APRs, late fees, and how interest is applied to existing balances. If avoiding surprise rate hikes is important to you, a card without a penalty APR may offer added peace of mind.

Stay on Top of Credit Card Terms and Avoid Penalty Rates

Staying informed and organized is your best defense against penalty APRs. Review your credit card statements monthly, keep track of due dates, and avoid charging more than you can afford to repay. These habits not only protect your interest rate, they also support your overall financial health.

Credit card agreements may change over time, so don’t assume the terms stay the same. Set a reminder to review your account terms at least once a year or after any issuer updates. A few minutes of planning can save you from months of costly interest.

Penalty APRs can catch you off guard—but they don’t have to. Sign up for Consumer Insite for clear, practical guidance on credit cards, interest rates, and smarter ways to manage your money.

Disclosure: Consumer Insite has partnered with CardRatings for our coverage of credit card products. Consumer Insite and CardRatings may receive a commission from card issuers.

Become an INsider and gain insight on more financial topics. We’ll

deliver resourceful content to your inbox.

By submitting your email, you agree to receive emails from Consumer Insite and partners.

Become an INsider and gain insight on more financial topics. We’ll

deliver resourceful content to your inbox.

Become an INsider and gain insight on more financial topics. We’ll

deliver resourceful content to your inbox.

Disclosure

Our first priority is to provide valuable information to help our readers gain insight into financial topics. Although we receive compensation from some of the brands listed on our site, we only highlight companies we believe can benefit our readers and their financial situations. Consumer Insite has partnered with CardRatings for our coverage of credit card products. Consumer Insite and CardRatings may receive a commission from card issuers.

Advertiser Disclosure

Our first priority is to provide valuable information to help our readers gain insight into financial topics. Although we receive compensation from some of the brands listed on our site, we only highlight companies we believe can benefit our readers and their financial situations. Consumer Insite has partnered with CardRatings for our coverage of credit card products. Consumer Insite and CardRatings may receive a commission from card issuers.

Become an INsider and gain insight on more financial topics. We’ll deliver resourceful content to your inbox.

By clicking submit you agree…

Disclosure

Our first priority is to provide valuable information to help our readers gain insight into financial topics. Although we receive compensation from some of the brands listed on our site, we only highlight companies we believe can benefit our readers and their financial situations.

Advertiser Disclosure

Our first priority is to provide valuable information to help our readers gain insight into financial topics. Although we receive compensation from some of the brands listed on our site, we only highlight companies we believe can benefit our readers and their financial situations.